This is an initiation article for Qingci (6633.HK) a mobile gaming company from China traded in Hong Kong. In this article, we cover why, using our proprietary algorithm to estimate revenue in mobile apps, we decided to buy shares from Qingci earlier last month and have it join our picks.

We’ll look at the company’s operations, its balance sheet and valuation and finally dive into the major catalysts in H2 2023 convincing us their upcoming earnings release is about to be a blowout.

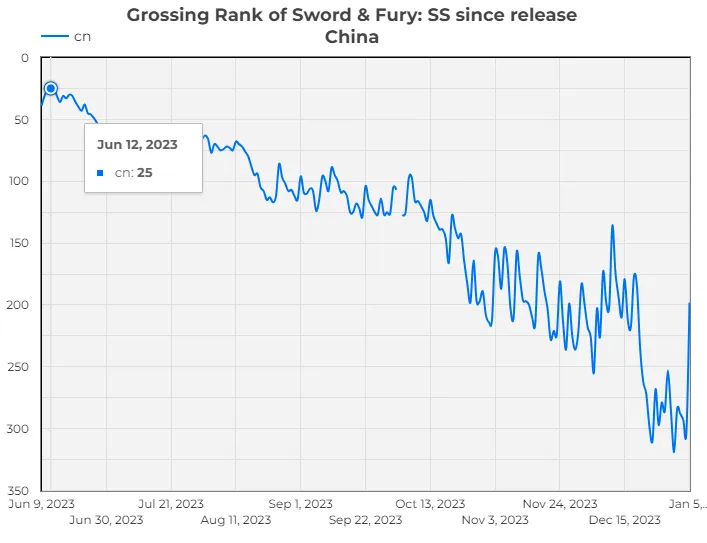

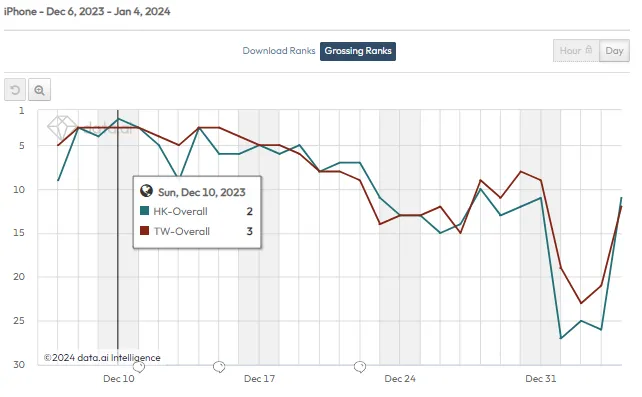

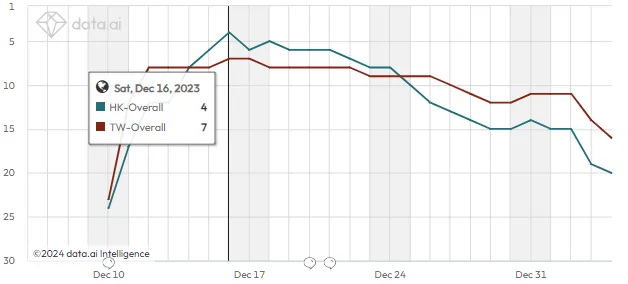

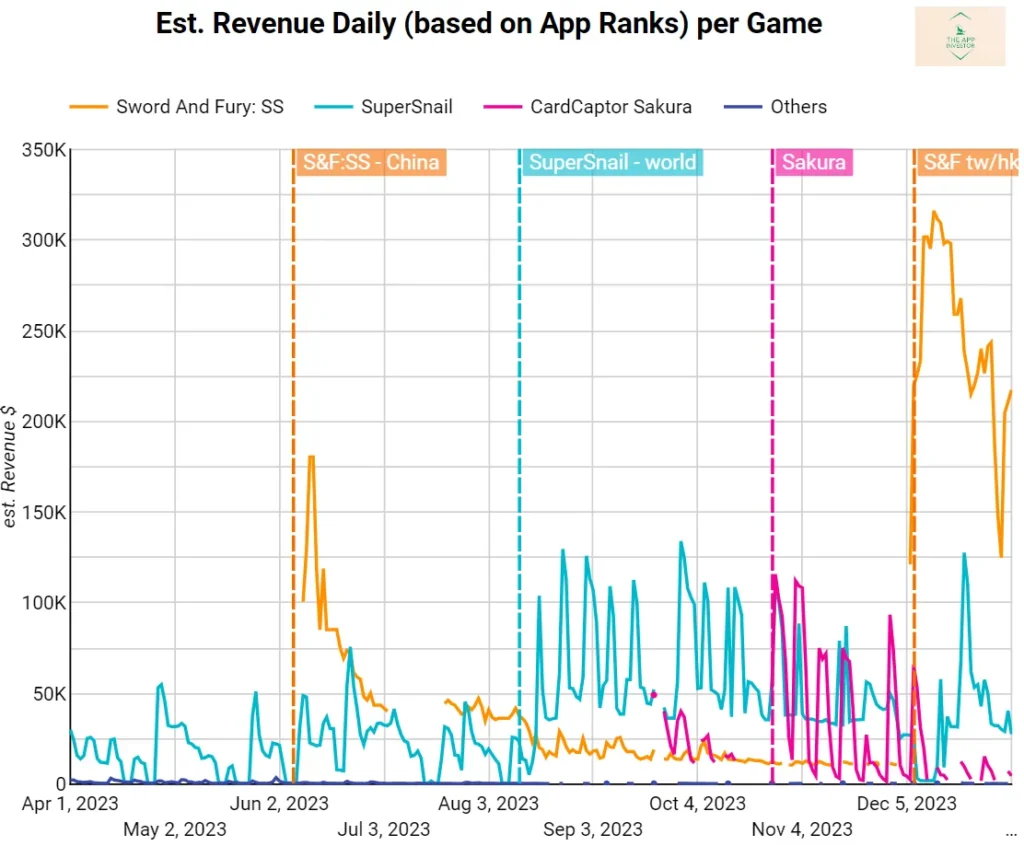

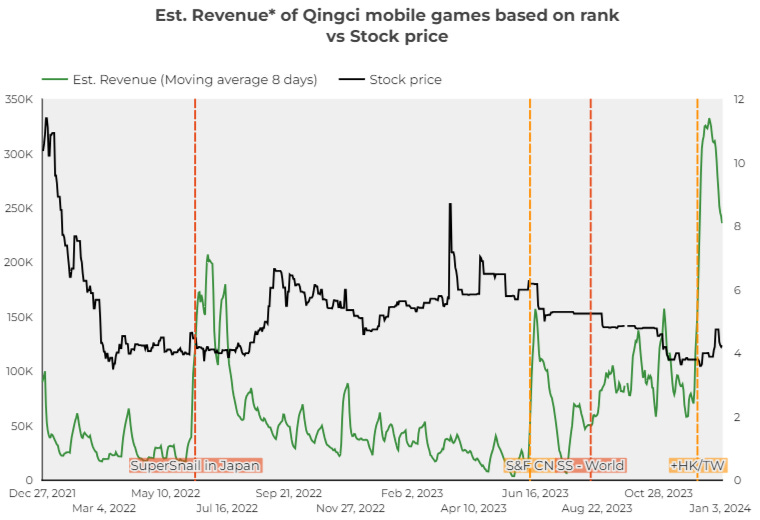

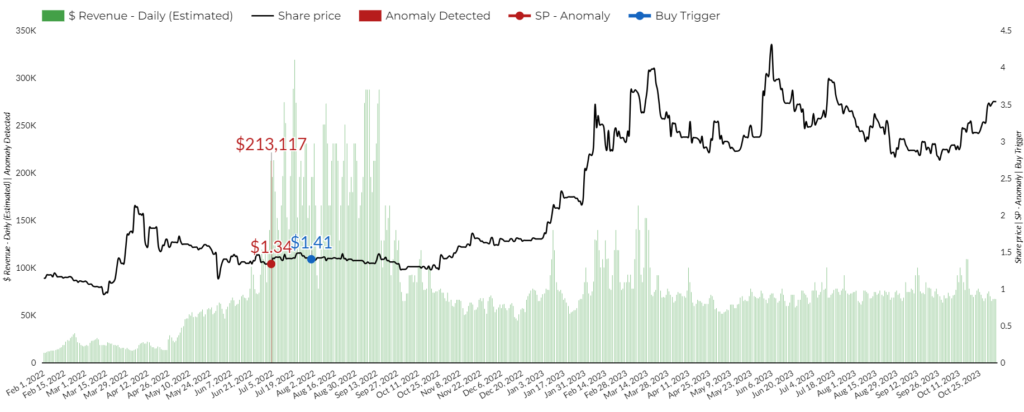

Now if we group all their mobile games revenue and look at the trend against the stock price, it is clear that they’ve hit the nail a few times, yet the stock only went down.

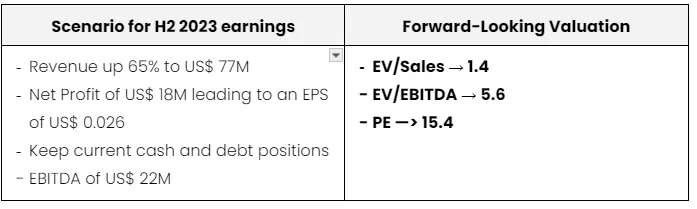

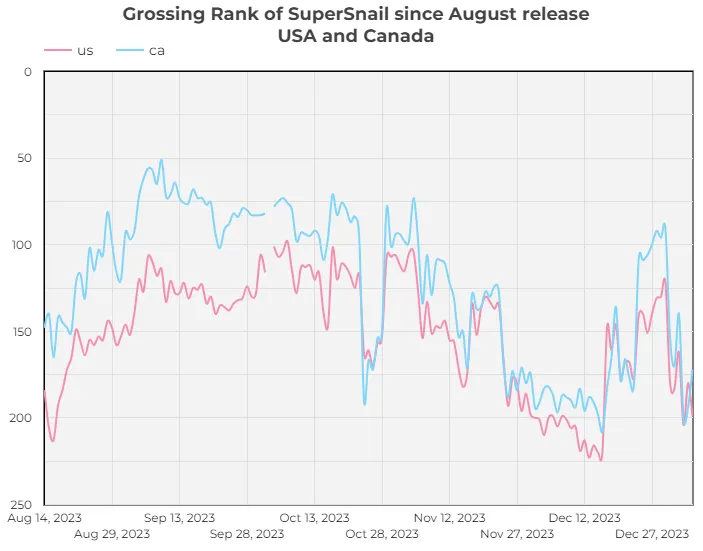

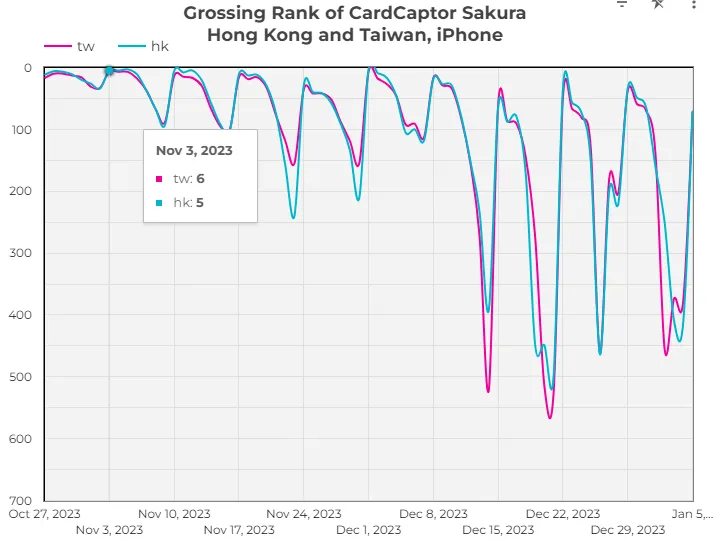

Beyond earnings, this could be the catalyst for a return to annualized growth, as they seem to have found their mojo back.

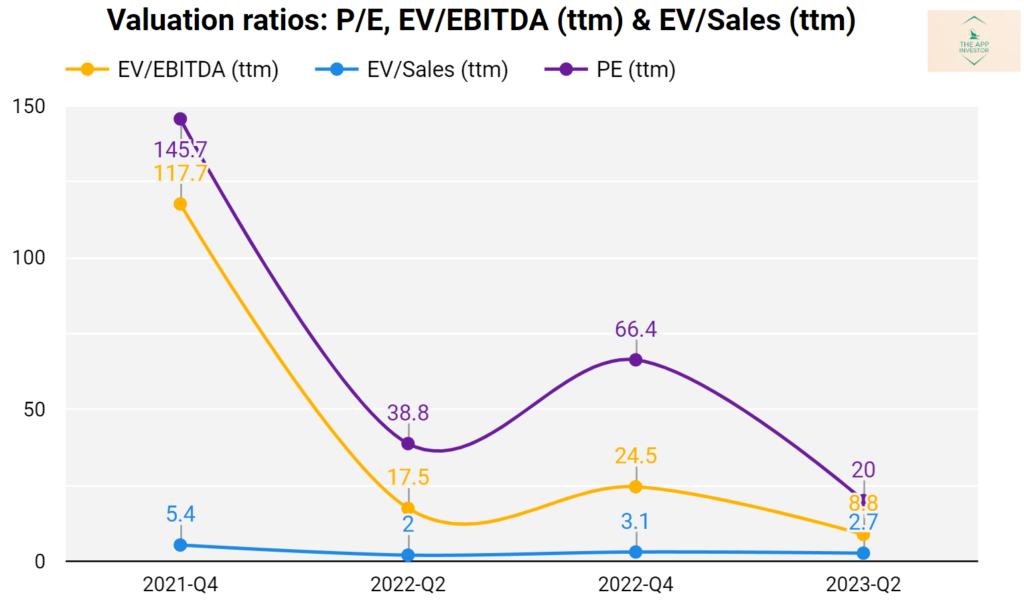

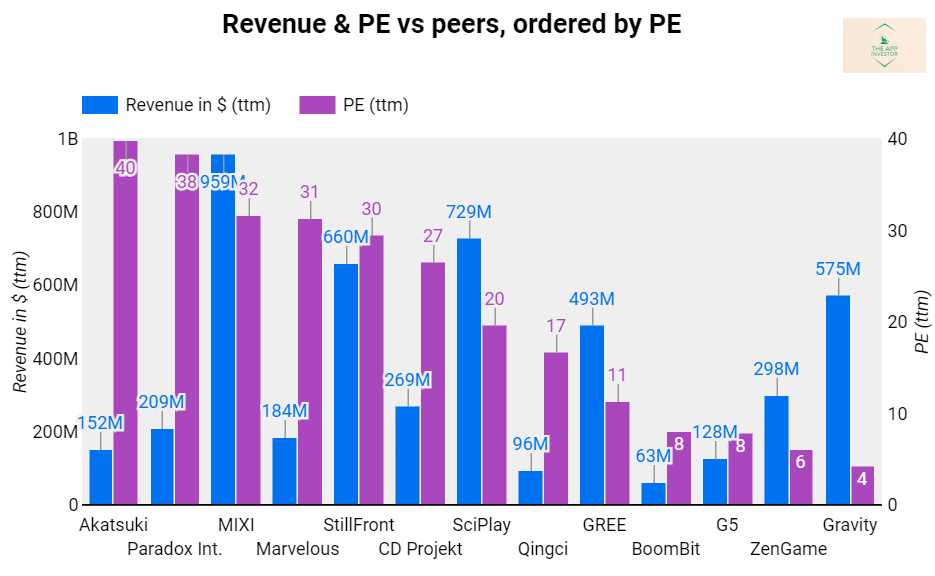

One can see how its valuation is steadily improving following the too expensive IPO. Altogether and compared with a field of peers that have relatively low valuation (we like value investing after all), Qingci’s valuation is middle of the pack today.

Here are our usual comparative charts looking at PE (with revenue plotted for sizing). We selected other companies based on size (revenues)

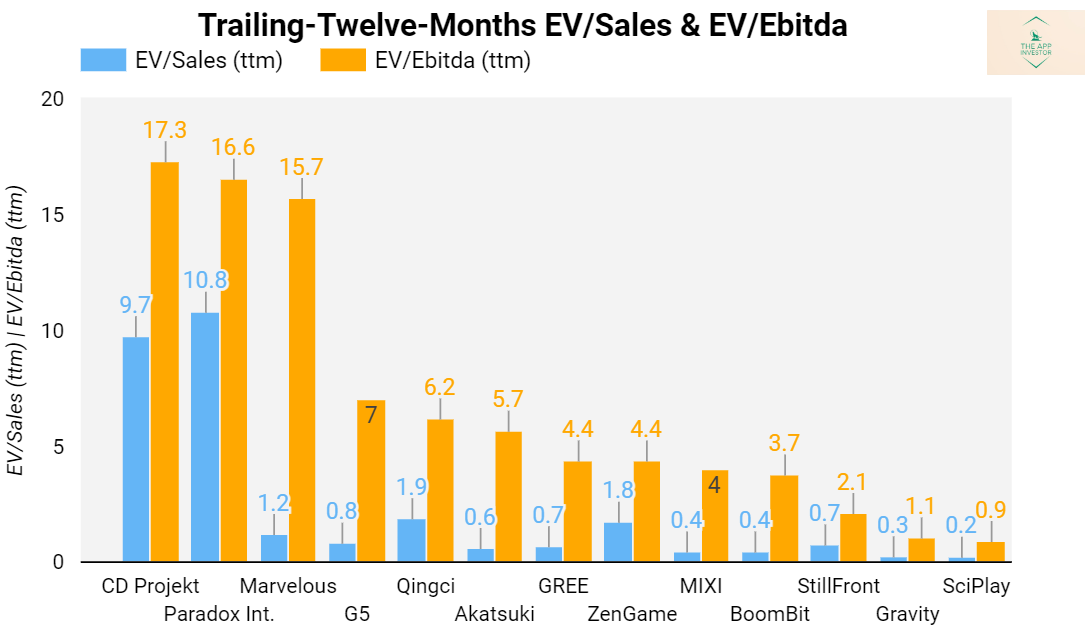

And the EV/EBITDA and EV/Sales comparison, where it sits close to other undervalued name out there.