Whilst we see limited upside given investor reaction to the earnings, we are keeping a position, given their very favorable valuation and the dividend. We would add to our position should they deliver another successful release this year.

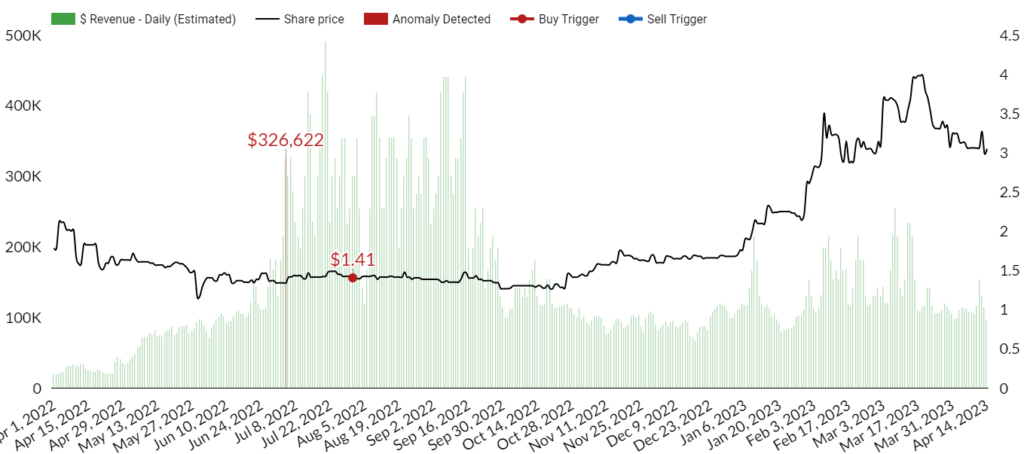

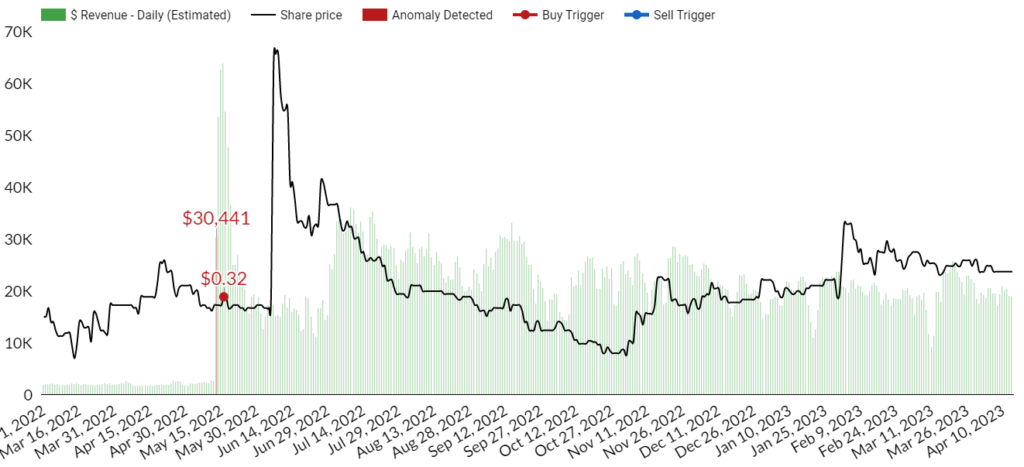

As usual, we share an updated snapshot of our estimates of Zen-Game’s revenue (green bars) against their stock (black line). Estimates only include iOS given Google Play does not exist in China.